Disability insurance is an essential form of income protection that provides financial security to individuals who are unable to work due to illness, injury, or a chronic condition. When considering disability insurance, individuals typically have two main options: employer-sponsored disability insurance and private disability insurance. Each option comes with its own set of advantages and disadvantages. In this comprehensive blog post, we will delve into the pros and cons of both employer-sponsored and private disability insurance, help you understand the key differences, and guide you toward making an informed decision about your coverage.

Understanding Disability Insurance

Disability insurance serves as a safety net for working individuals. It typically provides partial income replacement for those who cannot work because of a disability, allowing them to maintain their standard of living while recovering or managing their condition. There are two primary types of disability insurance: short-term and long-term.

Short-Term Disability Insurance: This type of insurance typically offers benefits for a limited duration, usually up to six months, and is designed for temporary disabilities, such as recovery from surgery or acute illnesses.

Long-Term Disability Insurance: This insurance provides benefits for an extended period, often until retirement age, and is intended for more severe disabilities that prevent individuals from working long-term.

Knowing the differences between employer-sponsored and private disability insurance is critical when assessing your options.

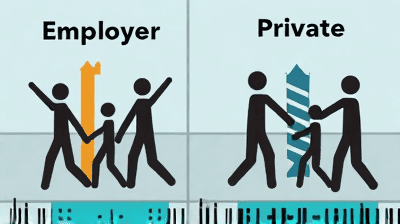

Employer-Sponsored Disability Insurance

Employer-sponsored disability insurance is coverage provided by an employer as part of an employee benefits package. This type of insurance may include both short-term and long-term disability options, and it is generally designed to help employees maintain income during periods of inability to work because of disability.

Pros of Employer-Sponsored Disability Insurance

Automatic Enrollment: When you start a job, you may automatically be enrolled in the employer-sponsored disability plan. This means you may not need to take any additional steps to secure coverage, which can be convenient.

Cost-Effective: Employers often subsidize a portion of disability insurance premiums, resulting in lower costs for employees. In many cases, the coverage can be provided at little or no cost to the employee, especially for short-term coverage.

Streamlined Application Process: Since the employer typically handles the application process, enrolling in the plan can be quick and simple. Employers may also assist with documentation requirements.

Guaranteed Issue: Employer-sponsored plans usually do not require extensive medical underwriting, so employees with pre-existing conditions may find it easier to obtain coverage compared to private policies.

Group Benefits: As part of a larger group, employees may receive better terms or coverage amounts than they would be eligible for in an individual policy.

Cons of Employer-Sponsored Disability Insurance

Limited Coverage Amount: Employer-sponsored disability plans often replace only a portion of an employee’s income, typically between 50 to 60 percent. This may not be sufficient for individuals with high living expenses, especially if this value is lower than the coverage provided by private policies.

Shorter Benefit Periods: Many employer-sponsored plans have shorter benefit periods, especially for short-term disability insurance. This may leave individuals without income support if they suffer from a long-term disability.

Job Dependency: If you change jobs or are laid off, you may lose your employer-sponsored disability coverage. This means that if you become disabled between jobs, you may not have benefits available.

Inflexibility: Employer-sponsored plans may not offer the same level of customization as private policies. Employees may have limited options for riders or additional benefits, impacting personal coverage needs.

Tax Implications: In some cases, if an employer pays for the disability coverage, the benefit payments received after a claim may be subject to income tax. It is worth understanding the tax implications of any employer-sponsored program.

Private Disability Insurance

Private disability insurance is coverage purchased individually from an insurance provider. Unlike employer-sponsored plans, private policies can be tailored to meet specific needs and preferences, providing an additional layer of security.

Pros of Private Disability Insurance

Customization: Private disability insurance allows individuals to customize their coverage to fit their incomes, needs, and preferences. This includes choosing benefit amounts, waiting periods, and policy riders that may enhance coverage.

Portability: Private disability policies are owned by the policyholder and are not tied to employment. This means that even if you switch jobs or become self-employed, your coverage remains intact.

Higher Coverage Amounts: Private policies often provide the option for higher coverage amounts than typical employer-sponsored plans. This can be beneficial for individuals with high incomes or those who have significant financial responsibilities.

Variety of Options: Individuals can shop around and compare various private disability insurance policies, allowing them to find the best terms and rates available in the market.

Protection Against Unforeseen Events: With private disability insurance, you are protected against any sudden job loss or changes, ensuring consistent coverage regardless of employment status.

Cons of Private Disability Insurance

Higher Premiums: Private disability insurance premiums may be more expensive than employer-sponsored options. Individuals may need to factor this cost into their monthly budget.

Medical Underwriting: Most private insurance providers require medical underwriting, which means individuals may need to disclose their medical history. Those with pre-existing conditions may face higher premiums or even denial of coverage.

Complex Application Process: The application process for private policies can be time-consuming and may involve extensive documentation to demonstrate the applicant's needs and health history.

Delayed Benefits: With private policies, the waiting period can vary. Some policies may have longer waiting periods before benefits begin, requiring individuals to have sufficient savings in place.

Market Variability: The availability of competitive rates and policy options may fluctuate, and it can take time to find the right plan that meets your financial and health needs.

Key Differences Between Employer-Sponsored and Private Disability Insurance

Cost: Employer-sponsored insurance is typically less expensive, as employers often subsidize premiums, while private policies usually come with higher costs.

Customization: Private disability insurance allows for a higher degree of customization compared to the typically standardized plans offered through employers.

Portability: Private policies are portable and remain with you if you change jobs, whereas employer-sponsored insurance is tied to your employment.

Coverage Amounts: Private disability insurance often allows for higher coverage amounts, thus better meeting the needs of high earners or those with significant financial commitments.

Waiting Periods and Benefit Durations: The specifics of waiting periods and benefit durations can differ, often providing more options with private coverage.

Making an Informed Decision

When deciding between employer-sponsored and private disability insurance, individuals should carefully assess their unique circumstances and needs. Here are several factors to consider:

1. Evaluate Your Current Coverage

Start by reviewing any existing employer-sponsored disability insurance. Understand its terms, coverage amount, waiting periods, and any deficiencies it may have in meeting your financial requirements.

2. Assess Your Financial Needs

Consider your monthly expenses and financial responsibilities. How much income will you need to maintain your standard of living if you become disabled? Look at your savings to determine whether you can manage an extended waiting period.

3. Consider Your Health History

Your health history and any pre-existing conditions should be considered, as they may affect your insurability and premium costs, especially when applying for private disability insurance.

4. Future Employment Plans

If you plan to change jobs or transition to self-employment, private disability insurance might be the better option, as it offers greater portability and ensures ongoing coverage.

5. Consult with a Professional

Seeking advice from an insurance agent or financial advisor can provide valuable insights. Experts can help you understand the complexities of both types of insurance and guide you to choose the right option.

Conclusion

Disability insurance is a critical component of a solid financial strategy, providing much-needed protection against unforeseen circumstances that can interrupt income. Both employer-sponsored and private disability insurance options have unique advantages and disadvantages that can significantly influence your decision.

By carefully weighing the pros and cons of each option and considering your individual circumstances, you can make an informed decision that ensures you have the right coverage to protect your financial future.

Whether you choose employer-sponsored insurance for convenience and cost-effectiveness or private disability insurance for its flexibility and comprehensive coverage, having a plan in place is essential for safeguarding yourself and your loved ones against unexpected challenges.